Student Loan Debt

What is Student Loan Debt?

The value of a college degree has never been higher – at least in financial terms. Over the past decade, the cost of a university education has risen three times faster than other school-related expenses. Most students finance at least some of that cost by taking out student loans, with the goal of having their investment pay off with higher earnings down the road.

According to the Federal Reserve, over half of young adults who went to college in 2018 took on debt. About 69% of students from the Class of 2018 took out student loans, graduating with an average debt balance of $29,800, according to Student Loan Hero.

Of those who are currently making payments, the average monthly payment is between $200 and $300, but roughly three out of 10 student loan borrowers are not required to make payments on their loans, often because of deferment. In 2017, 20% of those with student loans were behind on their payments, according to the Federal Reserve up from 18% in 2015 and 19% in 2016. Student debt has the greatest impact on Millennials, in part because they are the most educated generation in U.S. history. According to The Wall Street Journal, approximately 40% of those between the ages 25 and 37 hold at least a bachelor’s degree, compared to 25% of baby boomers and 30% of Gen Xers at the same age.

In the past decade, total U.S. student loan debt has surpassed credit card debt and auto loan debt. In the third quarter of 2018, Americans owed $840 billion on their credit cards and $1.21 trillion in auto loans. Currently, U.S. student loan obligations are larger than both, trailing only mortgages in scope and impact.

Student loan debt is a reality for more than 1 in 4 American adults. There are 44.7 million people with active student loans in the U.S., and the overwhelming majority of them are under the age of 60. The most recent figures from the U.S. Census Bureau estimated there are 171.3 million adults in America between the ages of 20 and 59. That means paying off student loans is a common challenge for 26% of younger adults under age 60.

The Growth of Student Debt

The costs for a higher education are among the fastest-rising costs in American society today. Since 1980, tuition costs at public universities has risen from $2,119 to $9,410, a jump of 344%. Private college tuition is up from $9,500 in 1980 to $32,410 in 2017, a jump of 241%. By comparison, food and electricity costs have risen about 150% and gasoline prices have risen more than 200% over the same period of time. A 2017 survey of Millennials found that 63% of them owed more than $10,000 in student loan debt and 42% of the women surveyed owed more than $30,000. Home ownership among those under-35 has dropped 21.2% since the housing collapse of 2009.

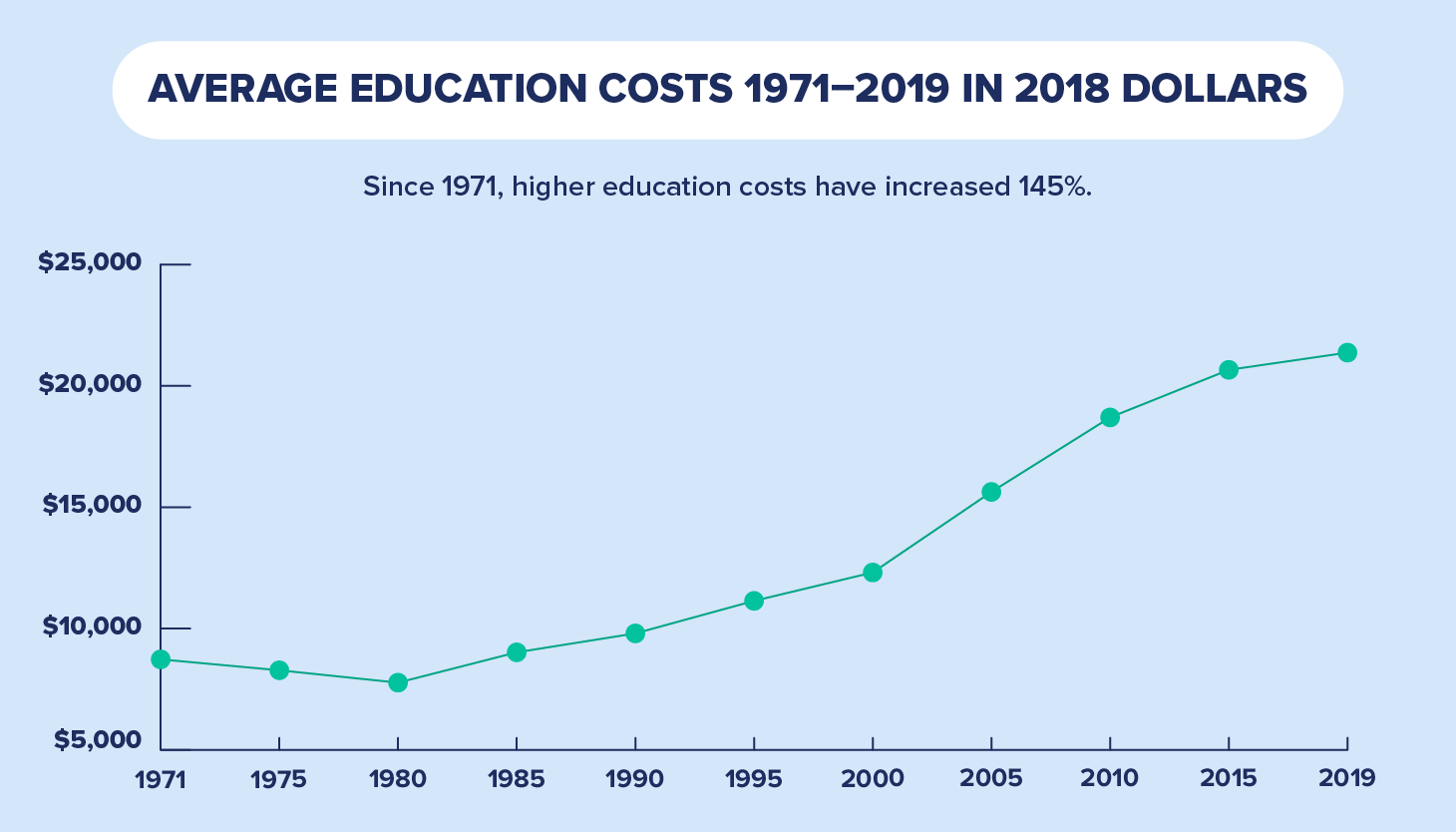

Student loan debt has ballooned in the past few decades, primarily because the costs associated with higher education – tuition, fees, housing, and books – have grown much faster than family incomes. The College Board has tracked costs at public and private universities since 1971. When the organization first started monitoring prices, the average cost of one year at a public university was $1,410 ($8,730 in 2017 dollars). That was 15.6% of the median household income of $9,027 and manageable for many families without going into debt.

Fast forward to 2018, and the picture is very different. Today, the average cost of one year at a public university is $21,370, which is 34.8% of the median household income of $61,372. That could be why more than 70% of bachelor’s degree recipients emerge from college today with substantial student loan debt, and why many find themselves in need of loan consolidation and refinancing.

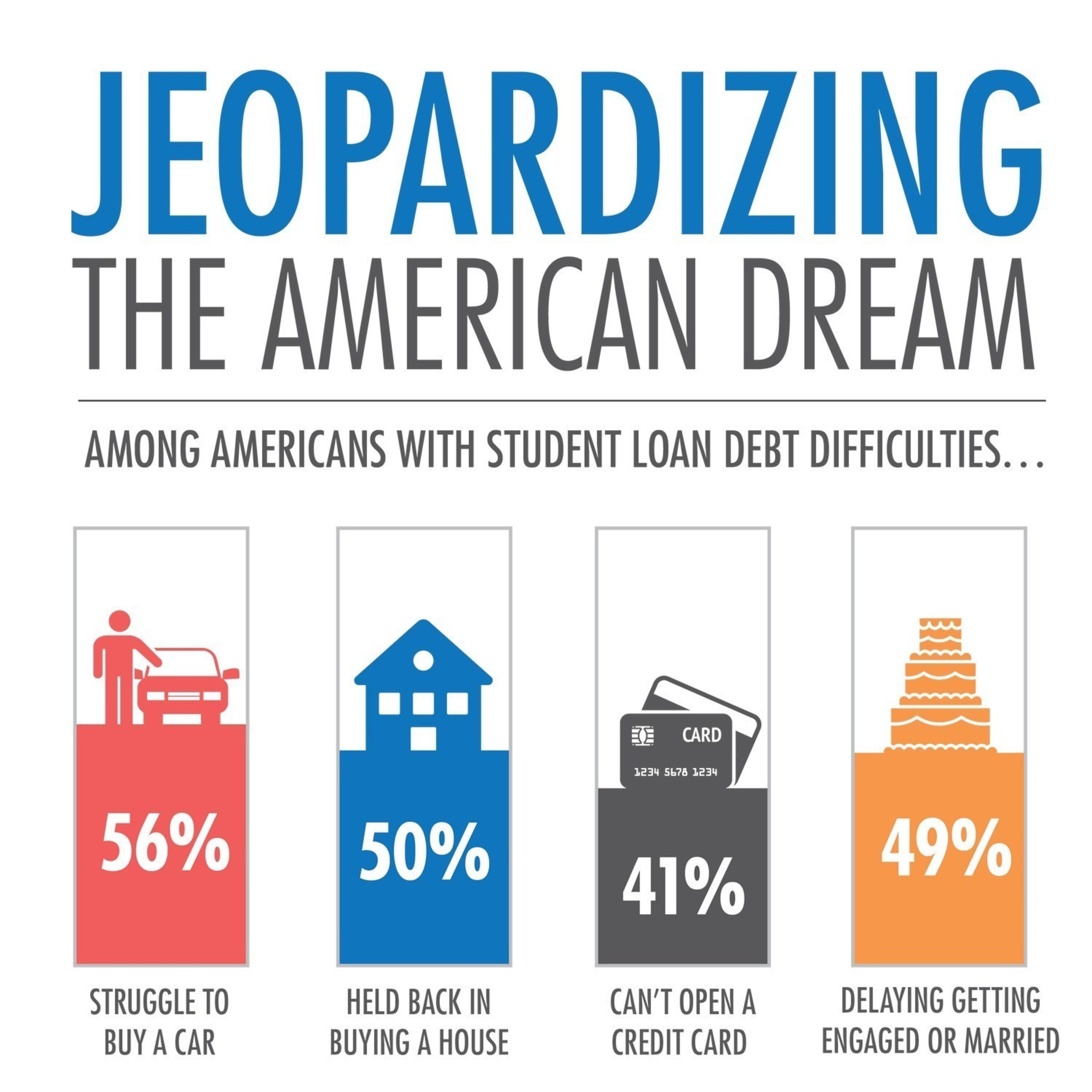

Impacts of Student Debt

There are many effects of student debt:

- Young graduates are avoiding starting a business

- Marriage rates are plummeting

- Millennials need twice as much retirement savings as their parents to maintain a comfortable lifestyle.

- People need to work more than one job and most don't live comfortably

- Graduates will spend less time thinking of ways to change society and more time thinking of ways to pay off their debt

Educational services company Cengage surveyed 2,500 recent and upcoming graduates for the Cengage Student Opportunity Indexand found that respondents, on average, believe it will take six years to pay off their student loans. In reality, it will take closer to 20. The Department of Education reports that the typical repayment period for borrowers with between $20,000 and $40,000 in federal student loans is 20 years, and a 2013 study of 61,000 respondents conducted by One Wisconsin Institute found that the average length of repayment for student debt borrowers is 21.1 years.

Today, only 51% of Millennial college graduates with student loans say that the lifetime financial benefits of their degree outweigh the costs.

Sources

Design Copyright © Christopher Lo 2019, Information from indicated sources