National Debt

How High is the Debt?

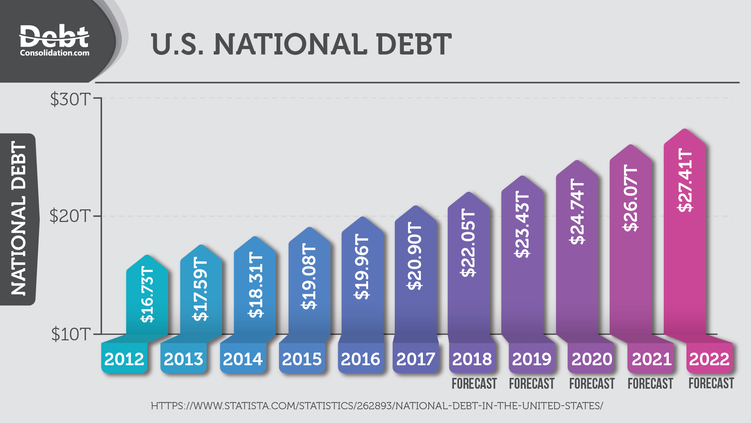

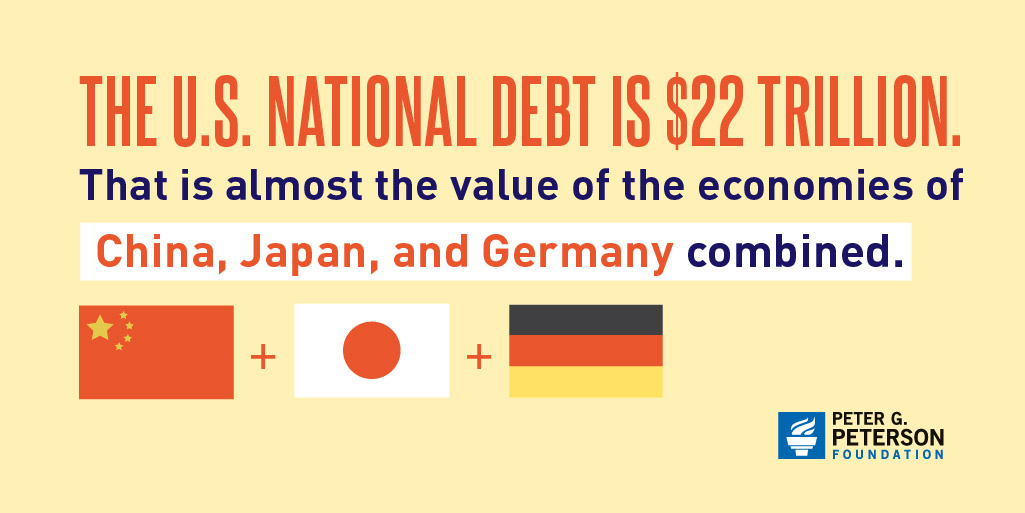

It is becoming fashionable to argue that federal budget deficits don't matter and that the government can undertake vast new spending programs without new taxes. This is not the time, however, to get wobbly about long-term fiscal policy. While it's not crucial to reduce this year's budget deficit, it still makes sense to phase in judicious spending reductions or tax increases that reduce long-term debt. The U.S. government's public debt is now more than $22 trillion — the highest it has ever been. The Treasury Department data comes as tax revenue has fallen and federal spending continues to rise. The new debt level reflects a rise of more than $2 trillion from the day President Trump took office in 2017.

Despite being in the second-longest economic expansion since the post–World War II boom, the U.S. is projected to rack up annual deficits and incur national debt at rates not seen since the 1940s, according to the Congressional Budget Office. Over the next 10 years, annual federal deficits — when Congress spends more than it takes in through tax revenues — are expected to average $1.2 trillion, which would be 4.4 percent of gross domestic product. That's far higher than the 2.9 percent of GDP that has been the average for the past 50 years.

Annual deficits and the national debt rose to new heights under the Obama administration, and the trend has continued under President Trump. As a share of the U.S. economy, the national debt stood at 78 percent of GDP in 2018. But the CBO says it will rise to 93 percent by the end of 2029. Again, those numbers put the ratio at levels not seen since just after World War II.

The national debt nearly doubled under Obama: It was $10.6 trillion when he took office and was nearly $20 trillion when he left. The rise has been blamed on factors from the Great Recession to wars in Iraq and Afghanistan and rising costs of Social Security and Medicare. Many of those pressures still exist. The CBO predicts federal spending will rise from 20.8 percent of GDP in 2019 to 23 percent in 2029, with programs such as Social Security and Medicare expected to spend more to cope with an aging population and rising health care costs.

The Congressional Budget Office forecasts the federal budget deficit will continue to increase this year and exceed $1 trillion each year beginning in 2022 and not drop below that through 2029. Addressing the long-term fiscal imbalance now does not require immediate, abrupt changes. Instead, we should phase in reforms to future spending and revenues. Social Security, where beneficiaries face mandatory 23% benefit cuts in 15 years in the absence of new legislation, would be a good place to start. The longer we wait, the larger and more disruptive the eventual policy remedies will need to be.

Why is There Debt?

Many factors contribute to the long-term outlook for the U.S. economy and budget, but in particular, there is a structural mismatch between the amount of revenues that the federal government collects and the amount of spending promised under current law. On the spending side of the budget, there are two major drivers of non-interest spending:  rising healthcare costs and America’s demographics. The primary driver of America’s long-term fiscal challenges is our inefficient healthcare system. America has one of the most wasteful healthcare systems among advanced nations. Combined with the demographic realities of a rapidly growing elderly population,America’s healthcare system leaves us with an unsustainable fiscal future. Not only will more Americans qualify for federal healthcare programs like Medicare and Medicaid, in the coming years, but older people, on average, need more healthcare. Consequently, without reform, the federal budget will bear the cost of rapidly growing healthcare bills.

rising healthcare costs and America’s demographics. The primary driver of America’s long-term fiscal challenges is our inefficient healthcare system. America has one of the most wasteful healthcare systems among advanced nations. Combined with the demographic realities of a rapidly growing elderly population,America’s healthcare system leaves us with an unsustainable fiscal future. Not only will more Americans qualify for federal healthcare programs like Medicare and Medicaid, in the coming years, but older people, on average, need more healthcare. Consequently, without reform, the federal budget will bear the cost of rapidly growing healthcare bills.

The United States spends $3.5 trillion — or 18 percent of the national economy — on healthcare. On a per capita basis, our healthcare system is the most expensive among advanced nations. Yet, America’s health outcomes are generally no better than those of our peers, and in some cases are worse, including in areas like life expectancy, infant mortality, asthma, and diabetes.

Impacts of Debt

The following summarizes several of the negative ramifications of our growing debt:

- Reduced Public Investment. As the federal debt mounts, the government will spend more of its budget on interest costs, increasingly crowding out public investments. Over the next 10 years, the Congressional Budget Office (CBO) estimates that interest costs will total $7 trillion under current law. In just under a decade, interest on the debt will be the third largest “program” in the federal budget.

- Interest costs, however, are not investments in programs that build our future. As more federal resources are diverted to interest payments, there will be less available to invest in areas that are important to economic growth. Although interest rates are currently low, we can’t expect that situation to last forever. As interest rates rise, the federal government's borrowing costs will increase markedly. By 2049, CBO projects that interest costs alone could be more than twice what the federal government has historically spent on R&D, nondefense infrastructure, and education combined.

- Reduced Private Investment. Federal borrowing competes for funds in the nation’s capital markets, thereby raising interest rates and crowding out new investment in business equipment and structures. Entrepreneurs face a higher cost of capital, potentially stifling innovation and slowing the advancement of new breakthroughs that could improve our lives. At some point, investors might begin to doubt the government’s ability to repay debt and could demand even higher interest rates — further raising the cost of borrowing for businesses and households. Over time, lower confidence and reduced investment would slow the growth of productivity and wages of American workers.

- Fewer Economic Opportunities for Americans. . Growing debt also has a direct effect on the economic opportunities available to every American. Based on data provided by CBO, income per person could increase by as much as $5,500, on average, by 2049 if we were to reduce our debt to its historical average of 42 percent of GDP. That amount would represent a six percent increase in income, compared to income if the debt remains on its current trajectory.

- The debt negatively impacts economic opportunity and social mobility because it crowds out investments that help Americans get ahead. Resultant higher interest rates would make it harder for families to buy homes, finance car payments, or pay for college. Fewer education and training opportunities would leave workers without the skills to keep up with the demands of a more technology-based, global economy. Faltering support for research and development would make it harder for American businesses to remain on the cutting edge of innovation, and would hurt wage growth in the U.S. Slower economic growth generally would also make our fiscal challenges even worse, as lower incomes lead to smaller tax collections and put the federal budget further out of balance. Vital safety net programs would come under even greater budgetary pressure, threatening support for those who need them most.

- Reduced Fiscal Flexibility. High levels of debt also reduce our government’s flexibility to respond to future emergencies, unanticipated challenges, wars, or recessions. Indeed, one reason why the United States was able to recover from the Great Recession more quickly than other countries was because our debt was fairly low — at 35 percent of GDP — before the financial crisis began. As a result, U.S. policymakers had considerable flexibility in addressing the crisis. If debt had been significantly higher at the start of the crisis — as it is now — it would have been difficult to respond. Similarly, the United States had the fiscal wherewithal to meet the considerable demands of fighting World War II because debt was relatively low before the war.

It is great news that Americans are living longer, and the retirement of the Baby Boom Generation comes as no surprise. However, these trends mean that the government will spend more on programs that serve this growing population of older Americans. In fact, spending on Social Security and the major health programs (which includes Medicare, Medicaid, the Children’s Health Insurance Program, and subsidies to purchase health insurance) accounts for all of the increase in federal non-interest spending relative to the size of the economy over the long term. These demographic trends are already putting pressure on the federal budget, threatening the sustainability of vital programs benefiting older and vulnerable Americans. A strong fiscal foundation can only be obtained by addressing the structural imbalance between revenues and spending — a result of our changing demographics and rising healthcare costs (as well as from interest costs on our growing debt). Understanding these key drivers of the debt is crucial to resolving our fiscal imbalance and improving our fiscal outlook.

Sources

National Debt is out of Control

National Debt Tops $22 Trillion for First Time

The Fiscal and Economic Impact

U.S. National Debt Hits Record $22 Trillion

Copyright © 2019 Geronimo Aldana unless otherwise noted